+91 99698 98000

+91 99698 98000

JUL-22 CPI INFLATION: SLIPS BELOW 7.0%

17 Aug 2022

KEY TAKEAWAYS

|

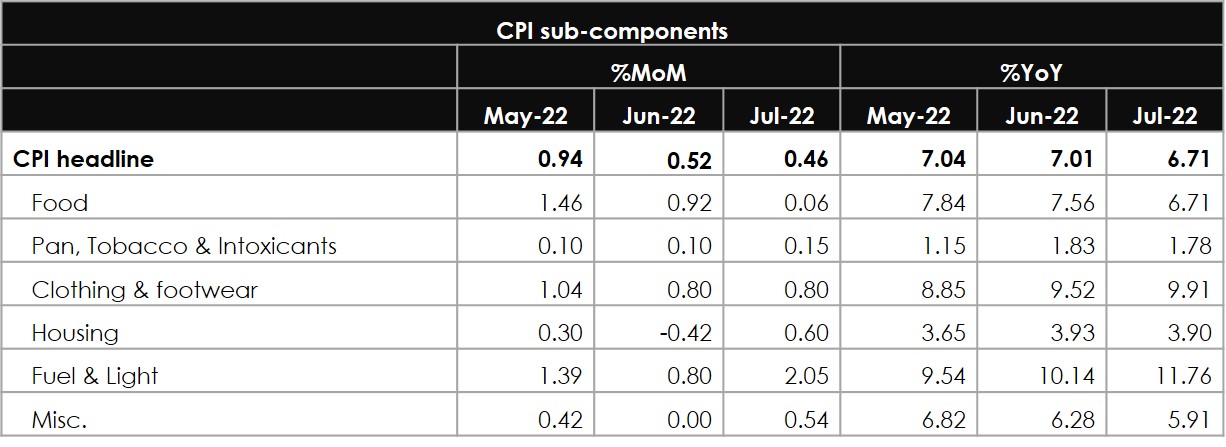

India’s CPI inflation moderated in Jul-22, to 6.71%YoY from 7.04% in Jun-22. This marked the first print below 7.0% in four months, and was broadly in line with market expectations (Reuters poll: 6.78%). After averaging at 7.3% in Q1FY23, we expect inflation to display some downside in the ongoing quarter, notwithstanding a marginal upward bias that months of Aug-Sep-22 carry, given an adverse base of the previous year.

Key highlights of CPI inflation

- Sequential CPI momentum eased further to the lowest level in 5 months, of 0.46%MoM in Jul-22 compared to 0.52%MoM in Jun-22 and an average of 1.11%MoM over months of Mar-May-22.

- Momentum for Food and beverages was substantially lower, at 0.06%MoM in Jul-22 compared to an average momentum of 1.28%MoM between Mar-Jun-22. The downside was led by a deceleration in price of Vegetables (-0.1%MoM, led by Tomatoes), along with Edible oils (-2.54%MoM) and Meat & fish (-2.92%MoM).

- In contrast, cereals momentum remained strong for the fifth consecutive month since the outset of the Ukraine-Russia war, primarily led by wheat and wheat products. As such, cereals inflation in Jul-22 stood at a near 2-year high of 6.90%YoY in Jul-22, nearly double of 3.46% from earlier this year in Jan-22. Going forward, the level of foodgrain stocks in the central pool will remain a monitorable.

- Consolidated fuel prices climbed up by a strong 1.53%MoM in Jul-22 with the impact of excise duty cut from May-22 waning out completely. While petrol and diesel prices eked small declines in Jul-22, sharp upward adjustment was seen in price of other fuel items such as Kerosene, Coke and LPG.

- Core inflation (CPI ex indices of Food & Beverages, Fuel & Light) momentum rose to 0.59%MoM in Jul-22, owing to a mean-reversion in Housing prices (after a seasonal dip in June), strong momentum in Clothing & Footwear along with a sizeable correction in gold and silver prices. While the annualized rate of core inflation remained above 6.0% in Jul-22, it has moderated to 6.04% from 6.22% in Jun-22.

Key highlights of WPI inflation

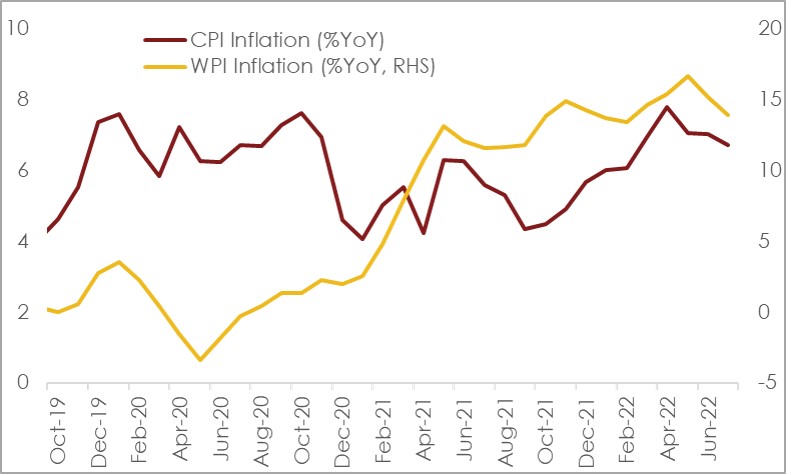

WPI inflation eased to the lowest level in 5-months in Jul-22, coming at 13.93%YoY compared to 15.18% in Jun-22. For the second month in a row, sequential momentum remained in contraction, the impact of which on the headline was exaggerated by a favorable base.

In our last CPI report in Jul-22, we had highlighted the abatement of two risks – one, softness in global commodity prices and two, recovery in Southwest monsoon after a sluggish overture. Both these factors continue to remain in favor of a moderation in inflation trajectory, so far in Aug-22. To put this in perspective, CRB Reuters commodity index has eased by nearly 12% since its peak in early Jun-22 while cumulative rainfall up to 15 Aug, 2022 remains in a surplus of 9% versus the long period average.

Despite this, we continue to maintain our CPI inflation estimate at 6.7% for FY23, due to the following reasons –

Chart 1: Both, WPI and CPI inflation moved lower in Jul-22

- At a granular level, momentum for both Primary articles (-2.69%MoM) and Manufacturing (-0.42%MoM) registered a deceleration, partially offset by a sharp increase in case of Fuel and power (+6.56%MoM)

- Within Primary articles, the decline was almost broad-based with the exception of minerals, as moderation in price of vegetables and other commodity prices (such as cotton, oilseeds etc.) aided lower food and non-food prices.

- Index heavy-weight manufacturing WPI contracted by 0.42%MoM in Jul-22, building on the deceleration of 0.90%MoM recorded in Jun-22. The decline was broad based with 12 of the 22 sub-sectors registering a correction in price, led by Wood (-3.57%MoM), Food (-1.53%MoM), Paper (-1.22%MoM) among others.

- In contrast, Fuel and power registered a strong sequential momentum of 6.56%MoM in Jul-22, more than reversing the 5.01%MoM correction recorded in the previous month. The upside was led by Diesel (+18.4%MoM), Kerosene (+17.4%MoM), ATF (8.6%MoM) and Petrol (+7.6%MoM).

In our last CPI report in Jul-22, we had highlighted the abatement of two risks – one, softness in global commodity prices and two, recovery in Southwest monsoon after a sluggish overture. Both these factors continue to remain in favor of a moderation in inflation trajectory, so far in Aug-22. To put this in perspective, CRB Reuters commodity index has eased by nearly 12% since its peak in early Jun-22 while cumulative rainfall up to 15 Aug, 2022 remains in a surplus of 9% versus the long period average.

Despite this, we continue to maintain our CPI inflation estimate at 6.7% for FY23, due to the following reasons –

- Impact of GST rate hikes on several food items of mass consumption (effectiveJul-22), along with hike in electricity tariffs by several states yet to get captured completely in CPI data.

- Pass-through of global commodity price correction on to CPI inflation is likely to be gradual and lagged. Further, the depreciation in the Rupee to the tune of 5.1%MoM on a FYTD basis stands to offset marginally some of these gains.

- Sowing of paddy in the ongoing Kharif season, as per Government sources, is lagging nearly 13% compared to last year owing to sizeable rainfall shortfall in key rice-producing states of Uttar Pradesh (-44%), Bihar (-39%) and Jharkhand (-36%). While Government’s rice stocks continue to remain above buffer norms, any shortfall in paddy production could put upward pressure on food prices.

- Services inflation could see an upside, amidst strong demand especially for contact-intensive services amidst complete normalization of economic activity.

Table 1: Key highlights of CPI inflation

Chart 1: Both, WPI and CPI inflation moved lower in Jul-22