+91 99698 98000

+91 99698 98000

JAN-22 TRADE DEFICIT: MODERATES ON OMICRON IMPACT

16 Feb 2022

KEY TAKEAWAYS

|

India’s merchandise trade deficit moderated to USD 17.4 bn in Jan-22 from an elevated level of USD 21.7 bn in Dec-21. Both exports and imports contracted sequentially in Jan-22 amidst the global and domestic backdrop of rapid spread of the Omicron variant.

For the first ten months of FY22, cumulative trade deficit stands at USD 160 bn, higher than USD 141 bn deficit seen in the corresponding pre-pandemic period of FY20.

Exports: Broad based decline

In value terms, merchandise exports moderated to USD 34.5 bn in Jan-22 from its record peak level of USD 37.8 bn in Dec-21. This translates into a contraction of 8.7% MoM - this sequential contraction on account of Omicron uncertainty is relatively moderate in comparison to the previous Covid wave in Apr-21 that saw a 12.8% MoM contraction in exports.

- Sequentially, the contraction was led by exports of Petroleum Products (USD -1.7 bn), Machinery Tools (USD -0.6 bn), Chemicals & Products (USD -0.5 bn), Electronic Goods (USD -0.3 bn), etc.

- Gems & Jewellery was the only major category that registered an increase (by USD 0.2 bn) in Jan-22.

Cumulative exports for the first ten months of FY22 stand at USD 335.9 bn, an expansion of 27.2 % compared to the corresponding pre-pandemic period of FY20.

Imports: Decline led by few key items

Merchandise imports eased to USD 51.9 bn in Jan-22 from its all-time high level of USD 59.5 bn in Dec-21, translating into a contraction of 12.7% MoM. At a granular level:

- Bulk of the sequential contraction was driven by imports of Petroleum Crude & Products (USD -4.2 bn), Gems & Jewellery (USD -2.5 bn), Transport Equipments (USD -1.0 bn), Chemicals & Products (USD -0.8 bn), etc.

- Meanwhile, import of Electronic Items, Machinery Goods, and Base Metals bucked the trend and posted a sequential expansion.

- While NONG (Non-oil-non-gold) imports, a key indicator of domestic demand, moderated by USD 1 bn, the overall magnitude of USD 37.6 bn recorded in Jan-22 is the second highest on record (with previous month level of USD 38.6 bn being the record high).

Cumulative imports for the first ten months of FY22 stand at USD 495.8 bn, an expansion of 22.3% compared to the corresponding pre-pandemic period of FY20, reflecting the pace of trade normalization despite the pandemic threat.

Outlook

The moderation in India’s merchandise trade in Jan-22 is a brief reprieve. Since it happened in the backdrop of escalation in most global commodity prices (barring fertilizers), the overall impact could be ascribed to lower demand, especially on the import front.

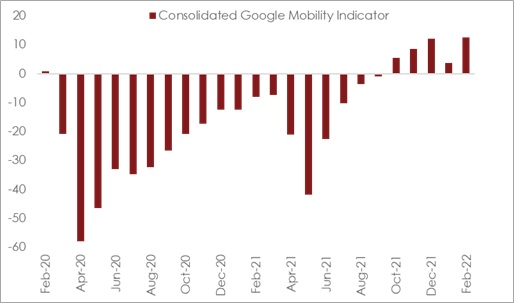

- While we don’t have volume data on imports yet, the 3.7% MoM decline in consumption (volume) of petroleum products in Jan-22 could be indicative of the broader trend in mobility disruption on account of Omicron, and hence overall demand for imports.

- Nevertheless, we note that the decline in consumption (volume) of petroleum products is shallower compared to the average monthly drop of 11.0% seen during the previous wave of Covid in Apr-May 2021. This points toward tapering of sequential economic disruptions from the pandemic amidst ongoing vaccination coverage, prevailing level of seroprevalence, and improvement in medical and healthcare facilities.

With the Omicron wave tapering at a rapid pace, states have begun to relax their lockdown restrictions. The test positivity ratio (on 7dma basis) has dipped from its peak of 17.6% on Jan 26, 2022 to 3.7% on Feb 15, 2022. If this declining trend continues, then the likelihood of near complete phasing out of lockdown restrictions in the next 2-weeks cannot be ruled out. This will once again stoke pent-up demand in the economy, which would also find support from year-end seasonality. Combined with the impact from elevated global commodity prices (esp. crude oil, which has jumped by ~23% in 2022 so far), we anticipate the pressure on imports to resurface.

A similar rationale would also benefit India’s exports, which seems poised to exceed government’s USD 400 bn target for FY22 comfortably.

On net basis, the merchandise trade deficit could remain elevated as the recent surge in global commodity prices would have an adverse impact on India’s terms of trade. Hence, if current levels of commodity prices hold (or increase further) in the near term, then our estimate of India’s current account deficit of USD 46 bn in FY22 could face a mild upside risk.

Table 1: Highlights of merchandise trade balance

Note: Numbers may not add up due to rounding off and revision in headline exports and imports

Chart 1: Global shipping rates, though still elevated, have started to cool down

Note: The consolidated indicator is an average of mobility changes on account of Retail & Recreation, Grocery & Pharmacy, Parks, Transit Stations, Workplaces, and Residential.